Debunking A Financial Myth

Why your retirement income target is not 70%

Why your retirement income target is not 70%

By: Frederick Vettese

If you have reached age 50, you might be getting a little nervous about whether you will hit your retirement income target. This will be especially true if you think your target is 70 percent of final employment earnings, the number that is most often quoted and indeed is practically taken as gospel in the financial planning industry. Fortunately for savers, that number happens to be wrong, at least for most middle to higher-income savers. There are many ways to show that the real target is less than 70 percent as is explained in in my book, The Essential Retirement Guide.

Perhaps the most compelling reason to believe in a lower target is that you never had the luxury of spending 70 percent of your income on yourself while you were working, so why will you need it after you retire?

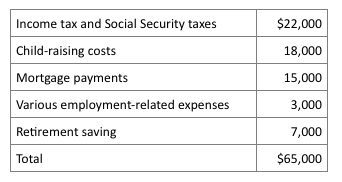

Consider the most common situation, a 2-earner couple with two children and a mortgage during the working years. If we assume the couple has combined employment earnings of $100,000 a year, Table 1 shows how they might be deploying their income in a typical year:

Table 1 – Breakdown of special expenditures

None of these figures is outlandish. Child-raising costs could be higher when various lessons, summer camps, and vacations are thrown in, not to speak of private schools. Mortgage payments in some parts of the country could easily be double the amount shown. The point, though, is not to show how extreme the numbers could be, but how surprisingly little is left for personal consumption even with a middle-of-the-road example.

In this case the couple is left with $35,000 for personal consumption, which of course translates into just 35 percent of gross income. To keep the example simple, let’s assume the couple continues to incur all these expenses right up until the time they retire. If all goes well, they would then get some relief if the children become self-supporting and the mortgage is finally paid off. In addition, employment-related expenses and retirement saving would obviously stop. As a result, all of their income in retirement (apart from a modest amount earmarked for income tax) can be devoted toward personal consumption.

With the $35,000 figure in mind and making some allowance for income tax, this couple might need $40,000 a year in retirement income to enjoy the same level of personal consumption they had during their working lifetime; a mere 40 percent of their final income!

Not convinced? You might argue that real life is not so cut and dried. For instance, what if the mortgage was paid off 10 years before retirement and the kids were also “off the payroll” by that time? In that case, you would have a lot more than 35 percent of your employment income available for personal consumption in your final few years of work. We will call these few years of high disposable income the Golden Years. In the above example, it would appear that you could increase your personal consumption to 70 percent during those Golden Years.

Or could you? During the early years when the child expenses and the mortgage hung like an albatross around your neck, you weren’t able to save enough for retirement. There is no way you could with personal consumption down around 35 percent or less. The Golden Years represent your last chance to make up for lost time by saving heavily for retirement. Doing so will eat heavily into all your disposable income so your personal consumption can never get up to 70 percent. If it does, it almost certainly means you’re not saving enough!

Besides having to save more during the Golden Years, think about the type of extra spending you will be indulging in with your disposable income. A lot of it will take the form of satisfying pent-up demand: the world cruise you always wanted, a mink coat or Rolex watch or maybe an in-ground swimming pool. The point is, this is one-off spending which you will not have to replicate once you’re actually retired.

In the case of the couple in our example, if they did manage to enjoy a few Golden Years, their true retirement income target might be 50 percent of final income after subtracting off extra saving and one-time spending, not 70 percent. Even at 50 percent, they are spending more on themselves than they did at any other point of their working lives, other than the Golden Years.

Another objection concerns low-income individuals. Surely they need to replace a lot more than 50 percent of their employment final income? I will concede that this is absolutely true and in Canada at least, the various sources of government pension will provide them with 100 percent or more of their final pay. The U.S. system is less friendly to low-income workers, which is why the poverty rate among seniors is so much higher in the United States than it is in Canada.

The final objection I will address here is the case of high-income individuals who never had children and always rented rather than buying their own home. In these situations, they will indeed have been able to spend about 60 or 70 percent of their pay check on themselves throughout their working lives and no doubt they will want to continue that pace after retirement. I will concede that people in this situation do indeed have a 70 percent retirement income target but they are a rare breed. Very few high-income people breeze through life without having to contend with mortgage payments or raising children.

Going back to our couple with a home and children, is it possible to manufacture a scenario in which their retirement income target is 70 percent? Certainly if they keep their personal consumption at 35 or perhaps even 30 percent for most of their lives so they can ratchet up their spending to 70 percent for a few precious years before retirement. This strategy sounds a little draconian to me but it might appeal to some people. For everyone else in the middle to upper-income category, the real retirement income target is closer to 50 percent than to 70 percent.

Frederick Vettese is Chief Actuary of the actuarial consulting firm, Morneau Shepell. This article condenses some ideas from his new book, “The Essential Retirement Guide: A Contrarian’s Perspective”, published by Wiley.

Category: Articles